Cost-plus pricing or cost-based pricing – a fixed sum or a percentage of the total cost of creating a product is added to its selling price.

>Download Now: Free PDF A Capability Framework for Pricing Teams

In the pricing and revenue management community, the term cost-plus pricing has increasingly come to have a very negative connotation. Some view it as a backwards-looking approach (see premium pricing strategy for a polar opposite).

In this article, we will discuss cost-based pricing in marketing and financial analysis. We will cover various cost-based pricing formulas such as companies that use cost-based pricing. We will also provide real-world case study examples. Also, we will evaluate a cost-based pricing approach, covering the advantages of cost-based pricing methodology and 5 valid reasons why cost-plus pricing is not the best option when making a business plan.

Table of contents for this article include:

I: Cost Plus Pricing: How to Use Cost-Based Pricing In Marketing

II: Pricing Methods: 5 Things People Say When They Do Not Get Pricing

III: Cost-based pricing strategy: Communication skills vital for pricing leaders

IV: Pricing System To Build A Culture of Collaboration In 100 Days

V: Distributor Pricing Model To Lock-in Cash & Capture Value In 2021-2022

Capability Building Programmes For Pricing & Sales Teams!

Using Cost-Based Pricing In Marketing

Cost-based pricing definition

I work in different environments where people are strongly committed to a cost-plus pricing approach and almost a badge of honour: i.e. the appearance (false in many cases) of financial rigour and numbers or financial accuracy gives them confidence. They are hard-nosed business people. However, often it can be a sign of anything but.

Numerous surveys of pricing teams and price diagnostics from consultants for both goods and services consistently show that the most commonly used starting point for an item’s price is its cost.

Issues of Cost Plus Pricing in the Forex Market 📉 Podcast Ep. 73!

A cost-based pricing definition is when the setting of a product or service initial price begins with a consideration of its costs.

There are many situations when a business may consider using cost-plus strategy examples to set or review their prices. They may need to come up with a new price for a product that does not already have a price or review prices for products that do have prices. In all of these situations, management arrives at an initial price for the item sold. Many choose a cost-plus or cost-based pricing strategy. Let’s find out why.

Cost-based pricing

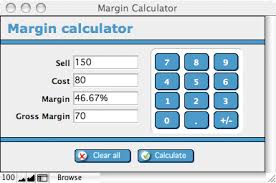

The logic of cost-based pricing is very simple. We get the item’s selling price by adding an amount of money (markup) to the item’s costs.

Cost-plus pricing

The simplest cost-based pricing method determines the amount added to an item’s cost and then adding that amount to arrive at the item’s price. This is a cost-plus pricing formula. If (C) an item’s cost; then its price (P) calculated as follows:

P = C + added amount

Companies that use cost-based pricing

A cost-plus pricing example is particularly common among companies that sell customised products, like construction materials, heavy equipment, parts, etc. Fletcher Building, Brickworks, Rinker Group, Hanson, Gunns, Adelaide Brighton and Nash Timber potentially all use cost-based pricing methods and formulas to some degree. Even energy companies and medical equipment or technology companies generally use cost-plus pricing strategy.

Cost-plus pricing construction

A cost-plus pricing example would be when a building materials business gives a price estimate for a job, by calculating its costs to do the job first (say $56,451). Key stakeholders at the building materials company meet to discuss how much they should add to this cost by considering factors such as the number of such jobs to do in a year, overhead costs, and desired final profits. Factors indicate that $32,987 added to the job’s costs; then the company would set the price of doing that job at $89,438.

Cost-plus pricing methods

Another form of cost-plus pricing example is mark up pricing. Mark up pricing used by businesses who buy lots of different goods and resell them at a fairly consistent pace like a distributor/wholesaler or retailer. They’ll have thousands of SKUs (Stock Keeping Units), products and many different product categories. Many commercial teams find it difficult to calculate the additional amount separately for each product (i.e., using the standard cost-plus formula as above). So, they often end up setting the price of an item using mark up pricing.

Markup pricing

Another cost-based pricing method is markup pricing. It basically adds to the item’s cost some standard percentage of that cost. The percentage used for a markup pricing formula could be the same for all of the company’s products. Alternatively, there is a separate standard percentage for each type of product sold by the company. Alternatively, a company has a separate standard percentage for each type of product that they sell.

Markup is the standard percentage used. The amount added to an item’s cost (C), expressed as a percentage of that cost. Below is how we calculate a markup (M) cost-plus strategy:

M = (added amount/C) x 100

Cost-plus pricing strategy examples

To calculate a retailer’s cost-plus pricing strategy example based on markup, the markup must first be converted into a proportion (by dividing it by 100) and then multiplied by the cost. The result of this multiplication is then added to the cost. This method of calculating a cost-plus price formula is written as follows:

P = C [(M/100) XC]

For example, to set your initial prices on a line of luxury biscuit boxes for Christmas, a retailer might apply a 200 per cent markup. If the retailer pays $8 for a particular brand of luxury biscuit box selection, it would use the following calculations to set a price of $24 for this line of luxury biscuit boxes:

P = $8 +[(200/100) X $8]

= $8 + (2.0 x $8)

= $8 + $16

P = $24

Cost-plus pricing method

A good question that I am sure you now have after reading this formula is what makes up the markups that companies use? A question so many procurement teams also ask these companies. For many distributors and retailers, markup levels are governed by tradition (they have always done it this way) or simple rules of thumb (a lot of rough estimates and guessing). In a wholesaling cost-plus pricing example, a typical markup on merchandise costs would be roughly 20%.

Keystoning cost-based pricing in marketing and merchandising

In retailing, fashion, gifts and food, they have traditionally used the so-called keystone pricing (or keystoning pricing method). Keystone is when a business doubles an item’s cost to arrive at its price (i.e. applying a 100% markup).

In the restaurant industry, the typical guideline is that the price of the items on the menu should be determined by tripling an item’s food costs (i.e. applying a 200% markup) and quadrupling the costs of served alcoholic beverages (i.e. applying a 200% markup).

An interesting point to note. When goods are passed hands more than once before reaching the consumer, successive markups are applied. A typical distribution channel for the biscuit example would have a markup story like this:

Manufacturer ($8 Manufacturer’s price)

Distributor ($8 cost to acquire + $1.60 (which is a markup of 20%) = $9.60 (final wholesale price)

Retailer $8 cost to acquire + $9.60 (which is a markup 100%) = $17.60

Consumers $24

This means the major retailer (like Coles and Woolies) is making $6.40 additional profit contribution dollars on every box of luxury business they sell; representing 80% of the manufacturers’ price.

Cost-plus margin pricing

Another form of cost-based pricing is cost-plus margin pricing or gross-margin pricing. Many businesses use cost-plus margin pricing because they want the process of calculating a price to be heavily influenced by the profit goals of the organisation. Many managers want to keep margins at a certain level of percentage so they meet their targets. Consequently, they set their product margins at a certain level aligned with their profit goals and work from there.

In contrast to a markup, which is the amount added to an item’s costs as a percentage of that cost, a per cent gross margin (or cost plus margin pricing) is the amount added to an item’s cost written as a percentage of the item’s price. Cost-plus margin pricing (or sales margin formula) looks like this:

%GM = (added amount/price) x 100

There are two ways to use a per cent gross margin to set a price

The first one is to change the per cent gross margin to a markup percentage because this often feels more intuitive (or easier). The second method is to calculate the product’s price directly from the gross margin percentage which would look like this:

P = C/[1 – (%GM/100)]

When the gross margin percentage is larger than the item’s price, it becomes considerably above the item’s cost. When it is small, the item’s price is only a little above the item’s cost. It is little wonder then, that you’ll hear many managers discuss high per cent gross margins (+30 – 55%) as the guideline they generally expect prices to conform to even in margin constrained businesses.

Big gross margin percentage means higher prices and more profit contribution dollars

Although the use of gross margins in the pricing setting helps to bring to pricing the influence of the selling organisation’s profit goals, the cost plus margin pricing method makes price review time a scary prospect. Many customers will ask for gross margin – markup equivalents to understand how you calculated your price rise. Some customers may be unwilling to pay a higher price. This happens if you have cost-plus pricing or a rule of thumb to back up your margin percentage calculations.

5 potential flaws with cost-plus pricing for your business

As mentioned, cost-plus pricing is particularly common among companies. However, there are also downsides in using this strategy.

1. How can you work out your costs?

In the classic case of cost-plus pricing, prices are set by adding a margin to the “costs”. The first real issue is a simple one – how can you calculate the costs?

This may seem a simple question. However, we have to decide what costs we should include. Is it total average costing, marginal costing, etc?

Think of a cost-based pricing example where a company sells 100 teddy bears (it is interestingly a teddy bear company – here is an example of a luxury branded teddy bear – Steiff.)

If someone doubles the order to 200 bears, what would the cost of the bear be for the calculation?

Should they set the price for the new bears at the average cost (i.e. dividing the factory, rentals, machinery costs, etc across the new bears)?

Also, should they reduce the cost for the original 100 bears as the same factory is producing more bears?

Or should it just be the marginal cost of the bears?

In an extreme example, if the marginal cost of bear production is zero, should they give that bear away for free?

We might have heard somebody say, “I have worked in companies where average costing was not giving us a ‘low enough’ price.”

What ended up happening, they started to remove costs that deemed as “not appropriate”.

2. What margin should you add?

If it is hard to work out costs, working out the margin or mark up to add is even harder in price setting. What is a good number i.e. 10%, 20% or 600%? Honestly, it can be whatever you want it to be.

3. Cost-based pricing gives a logical reason to not innovate.

This is a slightly funny way of looking at things but highlights the inherent flaws in this approach.

Imagine if you will, a teddy bear factory. There is a bright employee who comes up with a way to reduce costs by 80% without reducing quality. The management should logically reject this innovation if they are using cost-plus pricing.

Why? Because their profits would also drop by 80%. The markup percentage would still be the same (they would just be adding 10% or so to a much lower cost).

4. It does not recognise the value customers place on the product or service.

What if you have a really hot product or service? Wouldn’t it be foolish to ignore this when setting prices? The price of a beer would be almost the same in a dive bar as in the Ritz or the price of a business class seat on a flight would only be slightly higher than an economy seat (see blog on revenue management)

5. It gives customers the ability to push their prices down.

What if your clients in a B2B environment know that you are applying, say a 50% markup when their business only achieves 25% margins? They are likely going to use this to negotiate a price decrease.

I have been in meetings where customers have said, “We make 20%, so you are part of our supply chain and so you should not make any more than 20%.” It is never a good idea to give your clients an incentive to start these conversations.

With a cost-plus pricing strategy, you simply put a markup on your product to determine its selling price. This pricing method looks solely at the unit cost and ignores the prices set by competitors. Nevertheless, you’ll want to look at the benefits and drawbacks of this pricing strategy to determine whether it’s a good fit for your business.

Pricing Recruitment For Pricing Managers!

Points to Note:

There’s one big flaw with a strict full cost pricing. It destroys value. This is because an input price based approach leaves a margin on the table. You will be effectively underselling your commercial strategy. Re-pricing existing products once a price known. Make sure you get it right first. A price model that doesn’t consider issues like price competition will tend to be less profitable.

You must consider what value your product actually offers (and any differentiation). Then calibrate with your market price positioning versus your competitors. Things like monitoring price value differentials by product and segment are key here.

Whether you are in the Government Contracts game – or B2B sales, understanding the value your customers place on your product or service is key.

〉〉〉 Get Your FREE Pricing Audit 〉〉〉

A closing cost-plus pricing example

If you are the sole provider of a differentiated product, the cost to produce the service should really have no impact at all on the price you sell it at.

Value-based pricing is not about charging a higher price but pursuing a profit maximising pricing strategy.

Ask why the team is talking about full cost pricing at meetings. Especially if you are reviewing prices. Ask which cost added or if direct labour applied. Especially if you are trying to price a new product. You will soon realise you have a serious pricing problem.

If you would like to learn more about how to build a world-class pricing team for your business, download our complimentary e-book five ways to double EBIT or free pricing recruitment guides.

Don’t waste another dollar on the wrong pricing team strategy.

Capability Building Programmes For Pricing & Sales Teams!

Pricing Methods: 5 Things People Say When They Do Not Get Pricing

Pricing methods. How do you remove the misconception? There is a proverb from Geoffrey Chaucer that says, “Many a true word is spoken in jest.” Meaning, a humorous remark may turn out to be true after all.

In this short blog, we will take a lighter approach to highlight common misconceptions that pricing professionals often hear. This could even be thought of as a way to learn by asking questions – in the Socratic style.

Below are some of the common statements people say when it comes to pricing. We suggest you keep a bingo card and tick it off if you have heard of them. If you did, then you can give yourself a pat on the back. The next step and more challenging one is to try to win over the person to the side of pricing and revenue management.

Introduction to Price Optimisation 💰 Podcast Ep. 74!

How many of these statements have you heard before?

1. “You cannot just increase prices.”

This is one of the most common statements that you often hear. It is based on a fundamental misunderstanding of the pricing profession and pricing methods. Hence, we listed this one first. As if you cannot get past this one, you have no chance of getting buy-in with our implementing pricing optimisation. A good answer to this question will enable you to move on to more complex questions such as below. See our blog on premium pricing strategy.

2. “Is this some sort of pseudoscience with magic numbers?”

This one can come up or a variation on it when the concepts of psychological pricing, relative pricing, anchoring or numbers such as $5.99 are brought up. This should be viewed as a good thing as it opens the door for more discussion.

3. “Our sales force will never accept this price testing method.”

This is a great indication as to how the business is actually set up and who carries power. It can also give you great insight into why margin erosion may be appearing. At this point, it may be a smart idea to think about how sales teams are incentivised.

4. “You need to know our costs or drive our costs down more.”

This one follows directly from the one above – if not a sales-driven organisation, it may adhere loyally to a strict cost-based pricing strategy. Do the finance team have a large say in pricing strategy? This gives a great indication as to where your work should begin

5. “It will not work for us – as our industry is different.”

We left this one to last – as it is probably one of the most common comments. The funny thing is that we have not seen an industry yet where pricing improvements cannot be made.

We do not intend to belittle the common queries made by non-pricing professionals. Of course, they can be valid concerns when not answered with a clear and comprehensive solution.

Let’s explore what can be improved. Your sales team defines price as what’s on the invoice. The CFO defines price as ‘what we take to the bank’. Your customer says the price is too high. Your pricing manager says that price doesn’t match our standard terms. The distributor says they can’t make any money on your line. However, it’s still Monday morning!

So what defines and indicates price?

Can you improve net price realisation and take more money to the bank? I prefer price as what goes to the bank, after all, discounts, returns, warranties, commissions and other deductions before determining the final price.

There are several elements to price management. The first is achieving the optimal price for each good or service. The second is managing your product mix and services to achieve the optimal price for a set of customer transactions.

For many firms, the difference between what’s invoiced and what’s banked is over 10%, made up of co-op, early pay, volume rebates, freight allowances, returns and other factors, defined and imagined. The difference between list price and invoice price is often over 20%.

For a firm with a 10% operating profit, capturing a 1% price improvement falls through to operating profit and expands operating profits to 11%, a 10% improvement.

Do you spend as much time thinking about price as you do thinking about costs? We will discuss 6 things that you need to be attentive to that can help improve your pricing and profits.

Here are 6 steps to consider that can improve your pricing methods and profits:

-

Have a clear, executive-level pricing proprietor.

Most organisations do a great job of managing pricing execution and deals flow. Your pricing manager may be doing a good job tactically, however, they should also be thinking strategically. It is great to have a capable and experienced owner of pricing strategy who can think ahead into what to do more in the future.

According to a study published in the MIT Sloan Review, fewer than 15% of companies have any systematic pricing review.

What to do: Delegate one of your executive team, most likely the VP of Marketing or CMO, with building a pricing team and enabling them to develop a pricing improvement plan and process.

-

Optimise your product range.

Classify your customers and understand which ones are price sensitive. Have a basic price fighter in your range that will meet their needs without disrupting your full product line pricing.

What to do: Look at your product pricing methods vs. your user segmentation again.

-

Align sales compensation with profit growth.

If your reps are paid with basic wages (not for profits or price improvement), what incentive do they have to fight for the best price?

If you were selling and could make 5% commission on $1000 with little effort, or 5% commission on a $1010 sale with some effort and risk, what would you do? The 1% price lift is worth a negligible amount to them but a huge amount to your bottom line!

What to do: Consider having, at a minimum, your sales leaders receiving an incentive on the expansion of either average selling price or gross margin.

Pricing Recruitment For Pricing Managers!

-

Revisit your ‘price waterfall’ annually.

Check on all price deductions made prior to the final net price.

Are programs such as co-op still pulling their weight as you’ve shifted your pricing strategy to inbound marketing, pulling away from distributors to create demand? Do customers take an early pay discount when paying after the early pay period has expired?

Once you have established your price waterfall, compare it to your leading competitors. When you do, you are pushed to match invoice price plus you have more attractive trade terms. Oftentimes, your customers and sales team aren’t discussing in a price negotiation.

What to do: Conduct a review of you and your competitors, pricing methods, selling terms and price structure annually.

-

Understand your customers’ value.

Do those who set your prices truly understand your customers’ value? Do you have a pricing playbook and value pricing method which continuously reinforces the value of your products What diagnostic tool did your team use to improve pricing?

What to do: Ask your customers why they buy from you. This is a value discovery program.

-

Set expectations of annual price improvement.

Most businesses are worried about losing market share. Therefore, creating a culture of price improvement will ensure pricing is always top-of-mind for your commercial function.

What to do: Establish an annual price improvement goal and analyse on a regular period.

〉〉〉 Get Your FREE Pricing Audit 〉〉〉

Price optimisation is not about selling less at a higher price. It’s about eliminating the leakages and practices that enable you to capture improvement in a systematic way in your net price realisation. How much time do you or your team spend thinking about these questions? How much time is it worth thinking about to get a 10% expansion in operating profit?

In a very competitive business environment, companies need to capture the full value of their products. They can do it using different distribution channels in order to be successful. The good thing about focusing on the steps mentioned above is that they are very easy to implement and can start making profits almost right away.

See our blog on how pricing can help when making a business plan. Also, see our blog on 5 real issues with a cost plus pricing strategy and transformation pricing.

Capability Building Programmes For Pricing & Sales Teams!

Cost-based pricing strategy: Communication skills vital for pricing leaders

Why is communication a prerequisite for pricing leaders?

At Taylor Wells, we are often involved in the implementation of pricing teams and functions in businesses. Where they were previously or where they have not been seen as core to the commercial proposition of the business. This can be when the dreaded adherence to a faulty cost-based pricing strategy or cost-plus can be very strongly defended.

Among pricing, experts revile the cost-plus pricing for some legitimate reasons. For stand-alone projects, in particular, cost-plus pricing discourages efficiency and cost containment. When lower costs quoted, the company earns lower revenue and total profit. A bloated cost structure, on the other hand, will raise prices and boost profit.

Introduction to Price Optimisation 💰 Podcast Ep. 74!

Another is the cost-based pricing formula ignores both the customer’s willingness to pay and the competitors’ prices. Ignoring these factors would make pricing decisions entirely off base.

In this blog, we do not intend to cover any of the well-known weaknesses of a cost-based pricing strategy but instead touch on some of the pitfalls that can happen when a new pricing lead or revenue manager seeks to buy-in for a pricing optimisation program or movement towards value-based pricing. At Taylor Wells, we are ardent believers that a pricing leader is also a business leader, i.e. not a segmented function such as purely finance, risk or legal. If you really want to transform pricing in a large company, you need to win buy-in from sales, marketing, finance, the C-suite, operations. In other words, all departments. It’s not certainly easy to do this. We feel underappreciated sometimes with the task at hand.

How to broach the elephant in the room? Cost-based pricing strategy may not be the best way forward!

I was chatting to a friend the other day from a company where I used to work at. I was asking about the commercial strategy and who is setting a pricing strategy. He said, “How can they set prices when they do not even know the costs?” At that point, I do not have enough time to go down the road of explaining value-based pricing. Also, I do not want to criticise my friend who seems so committed to cost-based pricing strategy. Opinionated people exist. They stick to what they believe in. They see it as a form of hearsay or a lazy/shady marketing waffle when they hear anything different.

It can be an exhausting experience – winning buy-in from multiple functions for a move to value-based pricing. However, it is vital to build any pricing transformation. In fact, we view it as laying a solid foundation for the transformation. Otherwise, you are sure to find the optimisation program will flounder as if on quicksand.

There are sometimes strategic and tactical reasons to use cost-plus pricing. When implemented with forethought and prudence, cost-plus pricing can lead to powerful differentiation, greater customer trust, reduced risk of price wars, and steady, predictable profits for the company.

No pricing method is easier to communicate or to justify. Cost-plus pricing is inherently fair and nondiscriminatory to customers. That is if the business is 100% sure of its cost position. Most are not, however, and the cost base of products are often guesstimating rather than precision.

Cost-plus pricing is the very antithesis of value-based pricing, which seeks to discover differences between customers’ economic valuations and to exploit them by customizing prices.

Providing useful and understandable explanation and evidence on Cost-based pricing strategy

Taylor Wells commits to an education-based form of marketing pricing and pricing recruitment. We strongly believe in the ability of pricing to deliver sustainable profit and revenue boosts to even the most established business. When you are a pricing professional, the benefit of value-based pricing is almost self-evident. Still, we sometimes need to remember how we discovered the profession in the first place.

Usually, a light-bulb moment when value-based pricing becomes clear to us. The challenge in spreading the word to others is helping them have their own light-bulb moment. More often, the trick can make them believe that they thought of it themselves!

Pricing Recruitment For Pricing Managers!

Implications

Companies that use cost-based pricing stabilise price levels. These companies are less likely to engage in price wars if they base their prices mainly on costs instead of competitors’ prices.

Cost-plus pricing can encourage shoppers to use factors other than price in buying decisions. When consumers believe prices reflect cost, they are more likely to factor quality into their decision instead of just buying whatever is cheapest.

When the company has unique competencies that allow for an advantageous cost structure relative to competitors, it can use cost-plus pricing to create and deliver the most enticing value proposition of all.

〉〉〉 Get Your FREE Pricing Audit 〉〉〉

Conclusion

For companies with a cost advantage or an interest in using price transparency as a differentiator, cost-plus pricing is a powerful strategic tool. Companies are less likely to engage in price wars if they base their prices mainly on costs instead of competitors’ prices.

When implemented with forethought and prudence, cost-plus pricing can lead to powerful differentiation, greater customer trust, reduced risk of price wars, and steady, predictable profits for the company.

Undeniably, there are disadvantages to cost-based pricing such as it ignores demand and competitive situations. Nonetheless, companies find cost-based strategy attractive because it is simple and predictable. It is the most popular pricing method for service-based businesses. It ensures that production and overhead costs are covered. In addition, it assures a steady rate of profit for the business. This is a pricing strategy that guarantees a profit.

Capability Building Programmes For Pricing & Sales Teams!

Pricing System To Build A Culture of Collaboration In 100 Days

Pricing system: Our brains have hidden depths – and there’s a lot of untapped potential within us all. Whether it’s psychological tricks or proof of concept, our minds are biologically programmed to be receptive to external influences and cues.

Over the past few years, executive teams in Australia have found themselves wrestling with very meaty business problems such as pricing system issues.

They have been encouraging their teams to collaborate and embrace new pricing skills, team management skills, pricing system and practices to improve performance and in much shorter time frames.

Yet, dealing with a consistent stream of resistance and complacency from their people and customers has been a tough problem many businesses have not overcome.

For some executives, it was a no brainer, they were captivated by the pricing potential in the business and wanted to be the one who generated significant wealth for the business and its customers.

Introduction to Price Optimisation 💰 Podcast Ep. 74!

Many businesses were transitioning to the next phase in operations, and this in turn required a complete re-think of their current pricing system and sales operations.

The problem was, though, they also saw a proliferation of people problems attached to moving the business from cost-plus pricing system to more sophisticated pricing strategies and analytics.

Many gave up.

At first, CEOs and executive teams asked their managers and teams to work together to make the pricing project a success.

But often the message to ‘play nicely’ and accept new pricing practices were not getting through to the bottom line.

Teams across supply, pricing, sales and finance functions would resist or at best comply with broader directives to embrace more sophisticated pricing and sales strategies and analytics.

So, businesses started to recruit some serious leadership muscle and brainpower.

Pricing Recruitment For Pricing Managers!

What a smart pricing system can do

Instead of telling people to change their outdated thinking and pricing processes like it is their patriotic duty, smart leaders began trying to understand the psychological resistance to changing prices in the first place.

Most businesses found that value-based pricing was being labelled ‘consultant jargon’ by key leaders and influencers in the business – i.e., difficult to execute, right in principle but not in practice, etc.

They heard people say that dynamic pricing only works for airlines and would never work in this business…

Companies observed their sales, supply, operations and finance team’s insecurity surface as they began to change the most basic of operations and price administration.

So leaders started to launch campaigns to their peers, teams and stakeholders in an attempt to re-brand alternative pricing approaches as “pricing transformation.”

They also began to teach stakeholders and customers on how to think, feel and implement more sophisticated market strategies. They also re-framed their value relative to their customers’ key value drivers and better KPI’s (not just volume targets).

Once the sales teams started to see the results of reconnecting with customers using pricing as a device for wealth creation across the value chain, more teams became interested in working together to achieve collective goals.

Very quickly, the mission for all teams was to find innovative ways to deliver more complex business outcomes.

As more businesses and stakeholders within these businesses started to engage in the “pricing transformation,” resistance decreased.

Silos, turf wars and unhelpful patterns of thought diminished at the same rate as teams internalised better sales and pricing into their everyday thinking and routines.

Nowadays, value-based pricing is a management mainstay in leading ASX and FT 500 businesses and algorithmic pricing and AI are the new frontiers for optimal price and revenue management practice.

It may sound like a straightforward marketing campaign, but for today’s leaders, a subtle rebranding of pricing projects as a ‘set and forget’ practice to a ‘transformative learning’ process has gained status across industries.

When you associate pricing with transformative learning, you introduce 3 crucial psychological and pricing devices:

- psychological (changes in understanding of the self)

- convictional (revision of belief systems)

- and behavioural (changes in price practice and habits)

Taylor Wells observes some of the best leadership executives using some form of psychological intervention to identify and address a range of people and business problems, from team performance, change management, recruitment, to strategic planning and implementation.

People are your biggest asset and your biggest liability.

The cost of team underperformance for Australian businesses averages around $6 -7 billion dollars per year in lost productivity.

〉〉〉 Get Your FREE Pricing Audit 〉〉〉

Conclusion

Many businesses have not overcome the tough problem of dealing with a consistent stream of resistance and complacency from their people and customers.

Companies also saw a rapid increase of people problems attached to shifting the business from cost-plus pricing system to more sophisticated pricing strategies and analytics.

These days, value-based pricing is a management mainstay in huge companies and algorithmic pricing and AI are the new frontiers for optimal price and revenue management practice.

Capability Building Programmes For Pricing & Sales Teams!

The Best Distributor Pricing Model To Lock-in Cash In 2021-2022 🏪

What’s the best distributor pricing model for B2B firms selling and/or distributing products that are increasingly commoditised and competitively priced?

As markets change and whole industries are disrupted, the business models in the distribution sector are firmly in the process of continuous improvement. However, change is not consistent.

There are two types of business transformation happening in Australian distribution right now. The first comes from relentless commoditisation eating away at cash flow and profitability; basically last dash cost improvement exercises. For these businesses, it’s a fight for survival. The second comes from creating radically different business models and processes that are inherently value-based. These businesses are looking for innovation, growth and largely doing by establishing their value and worth using price and revenue/growth initiatives.

The distribution industry then is changing overall for the better. And, now more than ever, distributors are seeking to reconnect the business to their customers. Procuring higher-margin products and services that customers really need and value. Getting rid of stocks that are leading to soaring running costs. And pricing products and services at the optimal price rather than underselling themselves. Unfortunately, the success rate is still very low (70% fail).

In this article, we will continue to discuss the new distributor pricing model. We will look at how change and improvement are taking place at every corner of B2B distribution firms from procurement, finance, operations, strategy, product design & rationalisation, and IT upgrades. We argue that pricing – underpinned by a full investigated of value (internal / supply and value chain / go-to-market) – is the lever to capitalise on new B2B distributor value drivers while abating increasing and immediate competitive tension.

At Taylor Wells, we strongly believe that better people, value capture mechanism and price data analytics can help distributors achieve a competitive advantage and improve market share three times quicker than traditional methodology and approaches.

By the end of this article, you will learn the 5 best ways to capture more value using the latest distributor pricing model.

Issues of Cost Plus Pricing in the Forex Market 📉 Podcast Ep. 73!

Pricing: The Most Powerful Lever for Distributors

Pricing is the most powerful lever for increasing and improving gross margins and boosting profits for a distributor. In fact, a 1% increase in price across the product offerings has more effect on the bottom-line margins compared to a 1% rise in volume or a 1% decrease in procurement cost or in selling, general, and administrative (SG&A) expense.

Price is top of mind for most customer procurement teams so you need to ensure that your prices are right. Procurement teams focus on cutting costs, and they see your line of business as a means to do it. You need to demonstrate the value of your product portfolio. So that they don’t cherry-pick at line items and request excessive price reductions.

Unfortunately, most distributors struggle with striking a fair and equitable value exchange. The price data structures are commonly full of holes and skills shortages and unreliable and price complexity slows down vital progress. Especially for list price strategies and price optimisation purposes.

Take for instance a B2B distribution business we know that had more than 20,000 SKU items, 2,000+ customers and 5 different market groups. The possible price records were c.75 million. Though it is improbable that 75 million prices would be actually needed in commerce, this illustration shows just how complex the distributor environment can get without the right price management in place.

In the future, then, to be a successful distribution business, consider price optimisation. Price optimisation helps distributors sort out price complexity, but more importantly speeds up profitable revenue growth. Improving pricing helps sales teams generate more profitable sales and executive drive business strategy.

Overcoming Misconceptions: Key to Optimise Price

Skilled salespeople and even pricing teams still believe that increasing prices also means losing deals. Most especially if the competitors offer the same products. They may also argue for vigorous excessive discounting to make big customers happy and achieve their volume goals. However, the truth is more nuanced as revealed by qualitative and quantitative research.

So, how do pricing teams overcome these misconceptions and increase their win rates? Experienced pricing teams can improve their win rates with the best estimates of The Total Value to Customers (TVC). And by how much customers are actually willing to pay now for both commodity products and value items and offers. Some of which are: one-stop shopping in all categories, a wide range of brands and models, convenient and fast delivery, flexible return policies, financial assistance for small and medium-sized businesses, and product expertise.

The urgency for change is stopping margin loss. Reducing prices continually is a race to zero profit. In the long term, it’s more logical to create pricing tactics on each customer’s willingness to pay and then sharpen understanding of the non-price elements that the customer values most as team capability and understanding of customer value improves.

Building a Distributor Pricing Model to Create Value

Some distributors have been pioneers in embracing pricing as a discipline. A growing number have invested in establishing pricing teams with a directive to provide profit margin improvement every year. They are also developing price architectures that reinforce pricing discipline and link to pricing analytics and other tools or software to capture value.

We have identified 5 key components of creating an income-generating distributor pricing model. A model that builds considerable, steady increases in margins, even during the economic crisis:

1. Create a dedicated pricing organisation.

We know a major foodservice distributor in Melbourne, for instance, where discretionary pricing by sales and excessive discounting was widespread. The business was facing jaws of death situation and they decided to establish a new pricing team to help them control pricing and protect margin. However, integrating the new pricing team was not easy. It took the business a couple of years to create a streamlined pricing organisation with support in branches locally.

The pricing team reported to the chief operating officer and had a directive to steer annual margin expansion. They decided to gain support in the business and build credibility by launching quick-impact measures in pilot locations. Their approach was to create enough eagerness to start a pull from several branch managers instead of a push from the ivory tower. They got some traction, but there were also key lessons learned and not everything they did work.

However, after only 3 months, the pricing team was generating impressive incremental EBIT growth. The organisation invested more in its pricing team to further improve its capability. The foodservice distributor is now officially a revenue-generator (rather than a struggling distributor). They consistently generate between .5 and 1 per cent additional margin each year in their margin constrained segments and between, on average, 4 in their high growth segments. They have a reputation for performance with their customers and trusted strategic partners.

2. Use world-class processes in the pricing team.

Consider using best-in-class roadmaps, frameworks and inputs from pricing sales and marketing teams to define better pricing setting and management processes. This includes steps, owners, inputs, and outputs. From here, your business is in the position to achieve the thoroughness, structure, or oversight required for consistent profit maximization. Everyone is clear on what they need to do to achieve shared outcomes.

3. Adopt advanced analytics and digital transformation.

More than ever before, leading distributors are switching to advanced analytics to determine pricing opportunities. Using advanced analytics and embracing a digital transformation will improve the company’s margins significantly. Not only that but will also minimise human error and pricing variability. They should also establish pricing teams who in turn provide the business with evidence-based price guidance, benchmarks and data/quote tools to create better pricing decisions.

4. Tie sales with revenue and margin growth.

World-class sales organisations are tying compensation increasingly to both revenue and margin growth. But traditionally, the compensation of sales reps has been aligned to volume instead of margins. Sometimes leading to revenue growth at the expense of profit.

For example, we know an electronics distributor that was experiencing serious margin erosion in spite of solid sales growth. The company later discovered that its sales reps (that were solely compensated on sales growth) were offering free shipment and expedited shipping and reducing prices in order to “win” deals. However, a change in the compensation model and pricing strategies has improved both sales and margin growth.

5. Build trust and buy-in.

Building trust with sales teams can be achieved by getting results quickly and working with the right people. For example, working with general managers first to handle pricing initiatives in specific branches gets cut through much quicker than working directly with branch or sales. And then, once done with pressure-testing for impact, share results with the broader sales teams who in turn will ask you to roll out for them (rather you asking their permission). To build credibility within the broader sales-and-marketing function effectively, utilise general management in price trials and tests.

Discussion

Price improvement is not just a financial lever for immediate profitability. It is also a change management lever enabling B2B distribution to address the destructive issue of commoditization.

However, moving from a basic cost plus distribution pricing model to value-based pricing isn’t easy. It requires a value culture. Price management can be a big issue for distributors with thousands of SKUs and customer groups and multiple market segments. The combination of cost-plus and net pricing negotiations over time have created great deals of price complexity for B2B distributors. Which now, in turn, require much better price management and pricing-specific technology.

Higher calibre talent is highly sought after to ensure transitions to new models and ways of thinking are successful – and at every level and department in the business. In pricing for examples, distributors are now hiring high calibre pricing executives to redesign price architectures, transform cost plus thinking to value-based price setting, design performance rebates that grow share of wallet. And the reason behind this is strategic. Essentially better hires can think of better strategies to ensure the business get the full value they deserve. What’s more, they have the skills to implement a value-based business strategy. And here lies the secret of business longevity for distributors.

Pricing Recruitment For Pricing Managers!

Implications

- Distributors that undertake end-to-end pricing transformations can increase earnings up to 50% with little effect on volume.

- Sales teams can sell more and better. They not only issue more accurate quotes to customers, they also improve customer experience. Customers hate waiting for prices when they are ready to buy.

- Distributors’ value to the customer increases as the firm focuses more on improving their performance in areas that matter to the customer: i.e., supply chain, customer service, technical expertise, innovative products.

- Rigorous pricing processes reduce missed opportunities, minimise the risk of excessive discounting and impose global consistency.

〉〉〉 Get Your FREE Pricing Audit 〉〉〉

Bottom Line

Distributors work in a fast-paced setting. Oftentimes, they are processing thousands of deals and transactions each day. Everything should be quick and easy. But often it’s not. Managing inventory, supply and cost fluctuations can be a nightmare. Let alone, restructuring your pricing and revenue management to realise additional price premiums.

However, with the help of a good pricing team, distributors do move successfully from a trading business to a customer-focused business and margin growth occurs. Over time, they develop an effective price architecture that not only helps them manage prices but also focus on what matters to their customers.

Sometimes, success can mean winning mega-deals in high growth segments, but oftentimes success in pricing is under the radar and focused on the longtail of products and customers.

The pricing team, then, should support a distributor to implement the latest distributor pricing model to continually make more revenue and margin regardless of how commoditised or competitive the industries are and guide the business strategy on new growth opportunities in the best way possible.

Click here to download the whitepaper.

〉〉〉 Contact Us for a FREE Consultation〉〉〉

For a comprehensive view on integrating a high-performing pricing team in your company, download a complimentary whitepaper on A Capability Framework for Pricing Teams.

Are you a business in need of help to align your pricing strategy, people and operations to deliver an immediate impact on profit?

If so, please call (+61) 2 9000 1115.

You can also email us at team@taylorwells.com.au if you have any further questions.

Make your pricing world-class!